As we close the first quarter of 2026, Europe is once again reminded that geopolitics, economic prosperity and energy policy are inseparable. The war in the Middle East has sent fresh shockwaves through global oil and gas markets and disrupted less known but fundamental supply chains such as urea for fertilizer, sulfur and helium. But the lesson is unmistakable: on April 23, the EU had spent an estimated EUR 24 billion more on fossil fuels. As European governments seek to shield their citizens and businesses from these shocks, these measures are increasingly less fiscally sustainable: every Euro spent on fossil fuel support is one that cannot be spent on education, innovation, defense. Therefore, electrification - through renewables, storage and flexibility, stronger grids - are not only climate solutions, but they are also the backbone of the future European energy security and necessary. More than ever, the business case for cleantech is a business case for resilience.

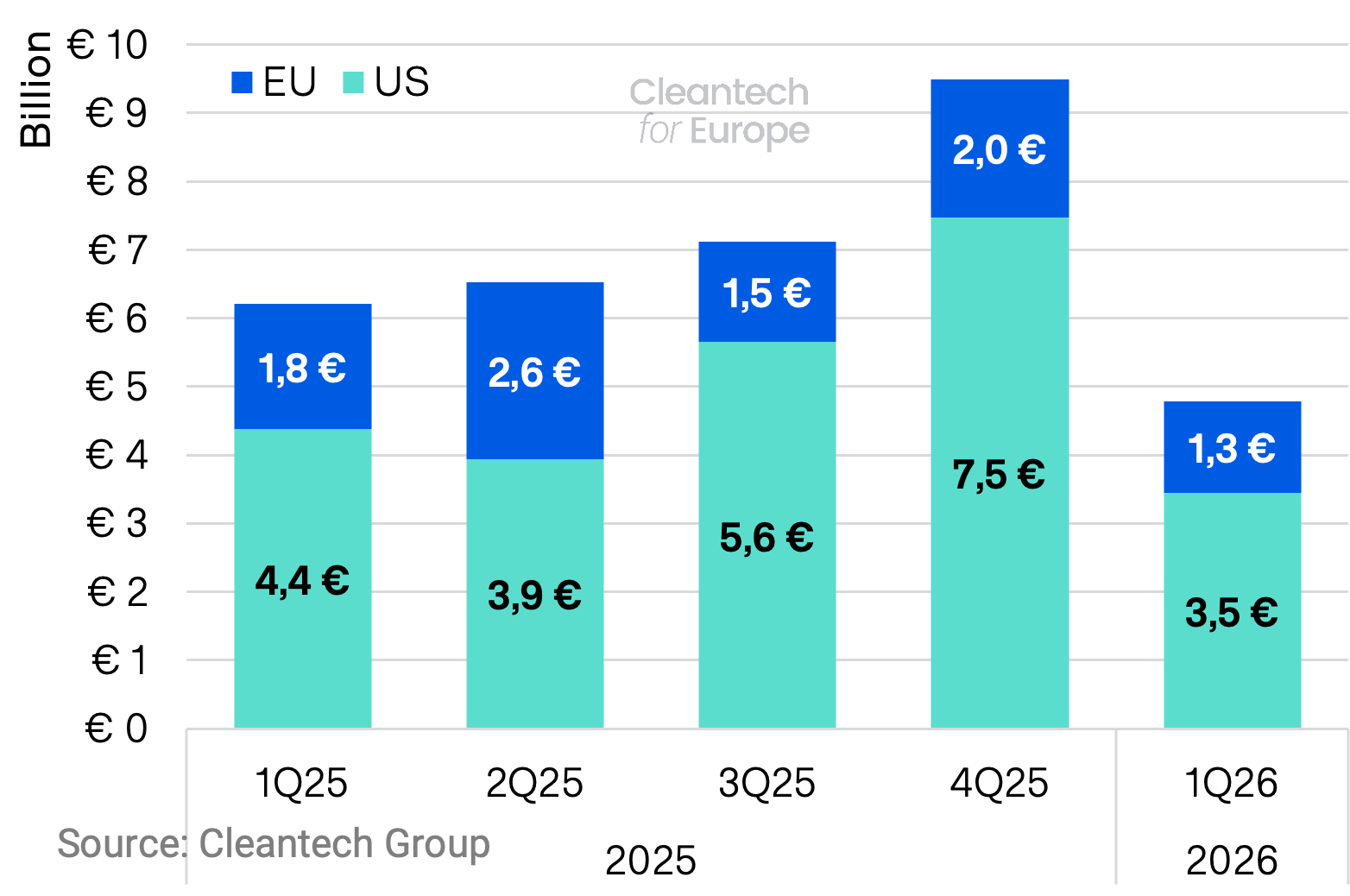

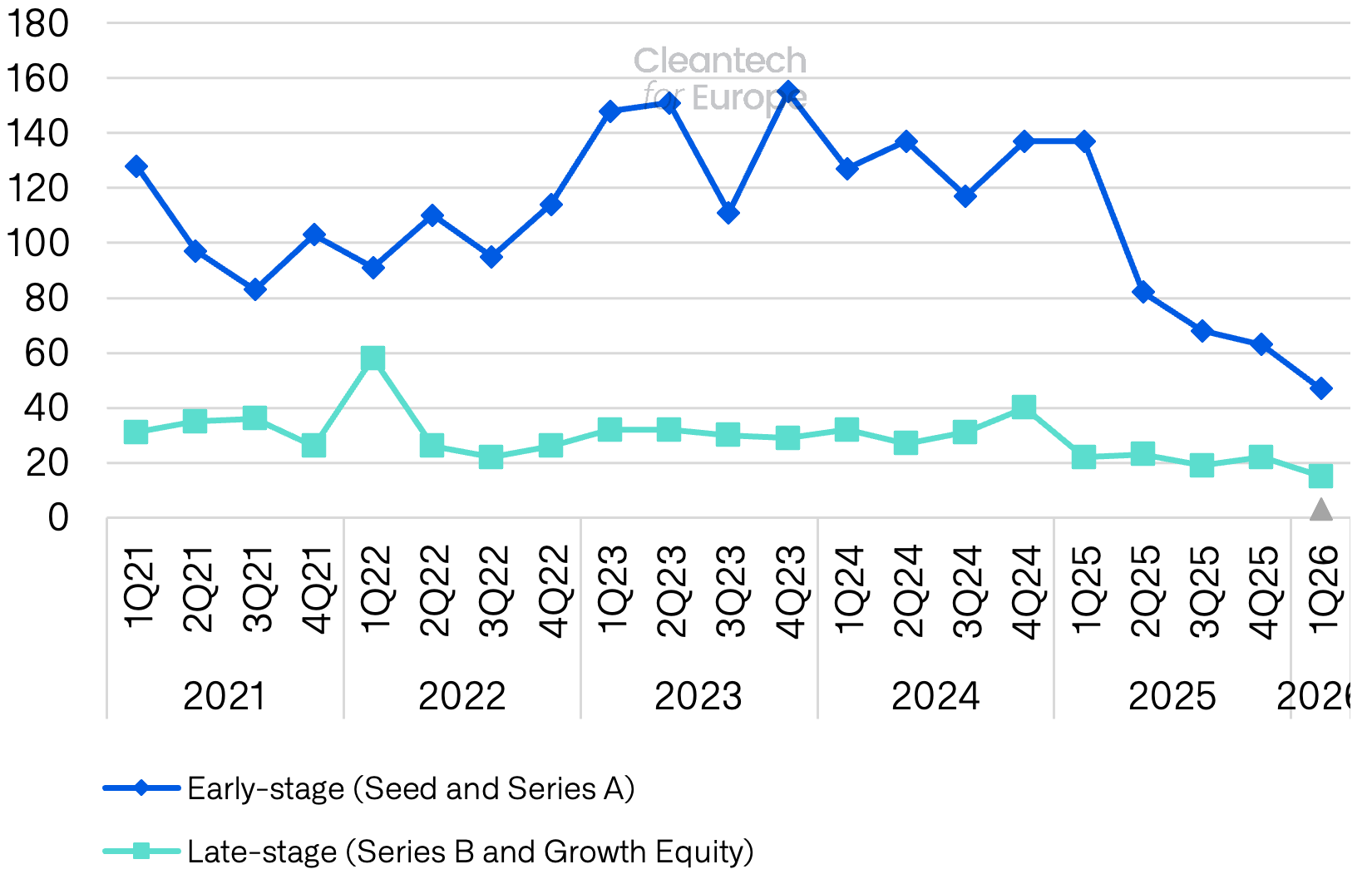

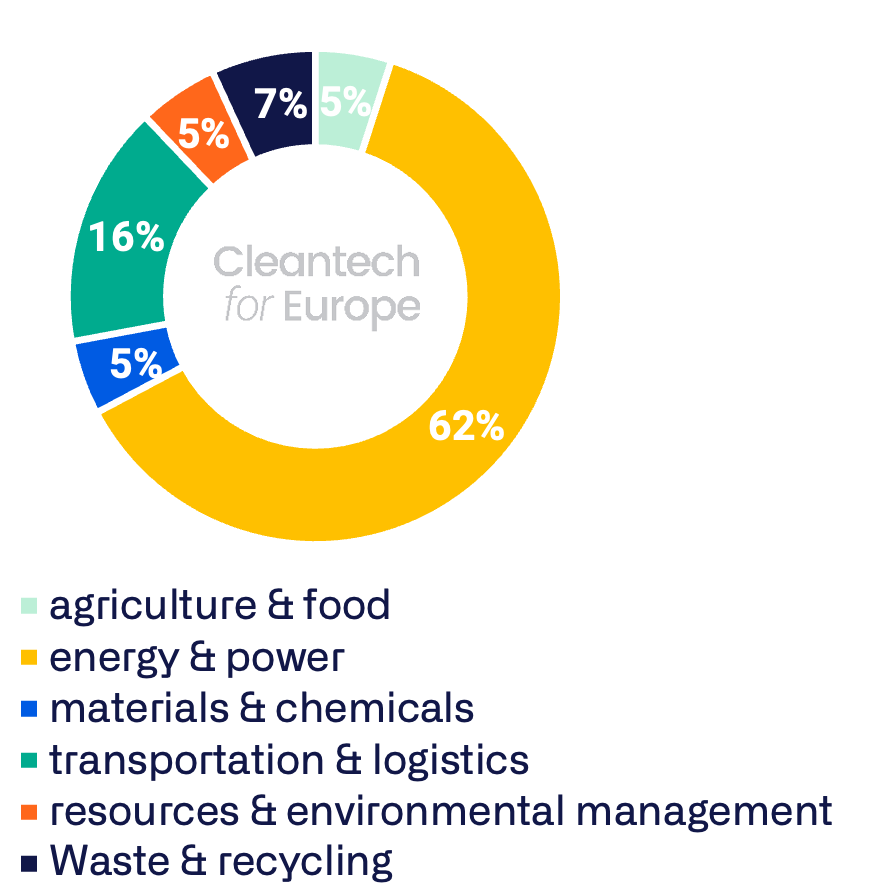

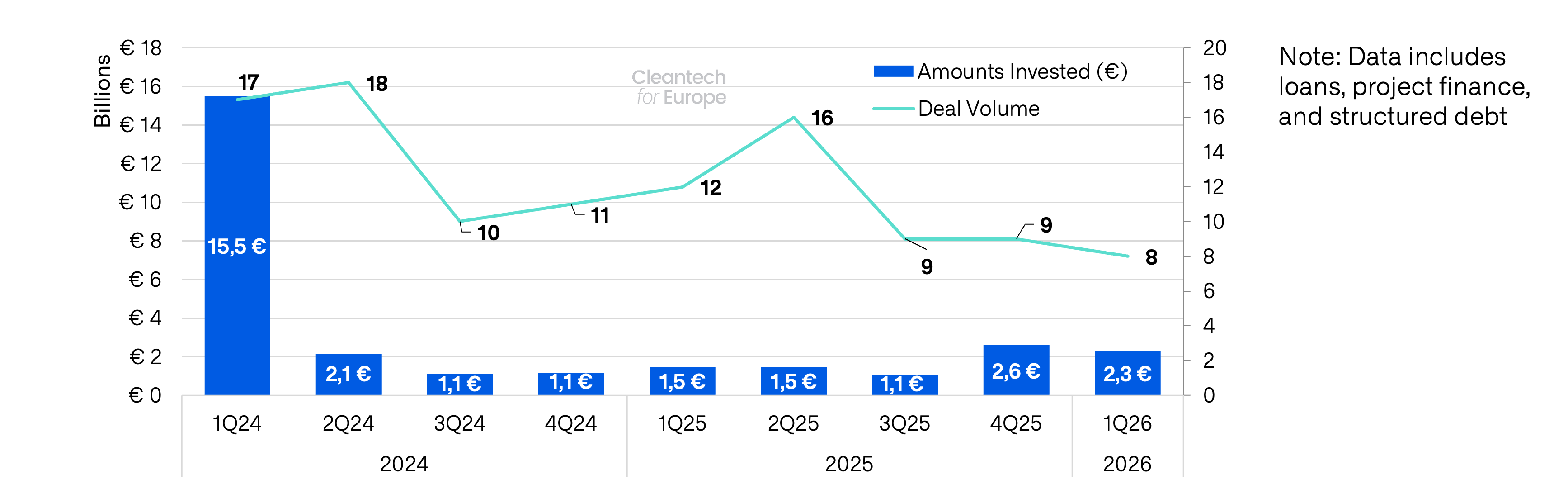

Against this backdrop, global cleantech investment has suffered from mounting macroeconomic headwinds: deep geopolitical uncertainty, the surge in fossil fuel and transport costs triggered by the Iran war, persistent inflation and a higher interest rate environment weighing on capital deployment. EU cleantech venture and growth investment fell to €1.3 billion in Q1 2026, down from €2 billion in Q4 2025 and well below the 2024 quarterly average of €2.2 billion. Total deal volume dropped to 62, the lowest quarterly count since 2017, with late-stage activity contracting to just 15 Series B and growth equity deals. The slowdown is even sharper in the United States, where €3.5 billion was raised across only 72 deals – the lowest since at least 2014 – with capital concentrated in a handful of nuclear and energy storage megadeals. EU investment has also become heavily concentrated in the Energy & Power sector. On the debt side, EU cleantech debt funding held up better at €2.3 billion across 8 deals, overtaking the US for the first time in recent memory as US debt collapsed to €2 billion amid tightening credit and rising private-credit default fears. Capital is also rotating toward technologies that decentralise resource systems and localise supply chains – long-duration storage, BESS, recycling, geothermal – while ESG-led segments like carbon removals lose momentum.

The structural weakness, however, is unmistakable: a persistent late-stage equity gap is preventing European scaleups from reaching commercial maturity and unlocking the larger debt rounds that follow. The EIB Group's launch of ETCI 2.0, targeting €15 billion to back around 100 European growth funds, and the upcoming Scaleup Europe Fund are welcome responses, but they must be deployed at speed and complemented by stronger institutional investor allocation to scale up capital.

On the demand side, the Industrial Accelerator Act (IAA) was meant to be the starting gun for a more assertive 'Made in Europe' industrial policy. But the final proposal is significantly weaker than earlier drafts: a narrower scope of local content requirements, generous escape clauses and an overly broad definition of "Union-origin" dilute the demand signal. China's late-April announcement threatening countermeasures against European trade defence tools, combined with its continued restrictions on critical raw material exports, makes it clear that timidity is no longer an option. Co-legislators must tighten the geographic scope to the EU/EEA with possibility of building partnerships with 'middle powers', close value chain gaps in batteries, grids and electrolysers, and build credible lead markets. Otherwise, they risk missing the reindustrialisation trajectory the IAA was designed to trigger.

The EU has responded rapidly to the energy shock. On 22 April 2026, the Commission unveiled AccelerateEU, addressing Europe's stark exposure (€340 billion in fossil fuel imports in 2025, plus €24 billion since March) with electrification at its core. The Grids Package, Electrification Action Plan and Geothermal Action Plan will be decisive to expand grid capacity, restore the investment case for renewables and flexibility, and unlock baseload capacity. Grid resilience is now a security imperative as much as an investment case: Ukraine has shown how exposed European infrastructure is to drones and sabotage, pulling intrusion-detection and grid protection into cleantech-core. Geothermal, in particular, must move beyond niche status: next-generation systems alone could generate 301 TWh annually in the EU – 42% of coal- and gas-fired generation – as domestic, attack-resilient firm power. And additional baseload has a systems value: it reduces the overall forecasted grids buildout.

These short-term measures will only be viable if the long-term direction holds. The crisis has prompted pushback from a few Member States on the EU Emissions Trading System trajectory. While the pressure is understandable, it must not derail the cornerstone of European climate policy. The ETS remains the most important driver of the cleantech business case in Europe; its predictability is what allows AccelerateEU's short-term tools to land. The two work in tandem, not in opposition. But it's vital that AccelerateEU is not limited to an 'electrification target' but focusses on a very accurate diagnosis of investment bottlenecks and has a concrete strategy to unlock these and unlock the necessary enabling measures.

Finally, we had the pleasure of hosting with the Cleantech Friendship Group the IEA to present its Energy Technology Perspectives in Brussels. What came out of it is an uncomfortable fact the EU will need to address head on: energy security dictates the EU moves fast on electrification. But any electrification scenario will, in the absence of industrial policy step change, grow the EU's technological dependency on China. The EU has a very careful balancing act to perform: reduce a dependence on imported fossil fuels without sleepwalking into a dependency on imported technology.

.webp)

-min.jpeg)