As Europe enters 2026, it is worth stepping back and situating today’s cleantech debate in its proper historical context. Headlines often focus on the recent slowdown in venture and growth investment, suggesting a sector in retreat as the low-interest-rate environment of 2021-22 fades and topline investment levels in 2024 and 2025 remain below early-2020s peaks. Yet when viewed over a full decade, the picture is very different: cleantech investment levels throughout the 2020s – including in 2025 – remain far higher than the annual averages of the latter half of the 2010s.

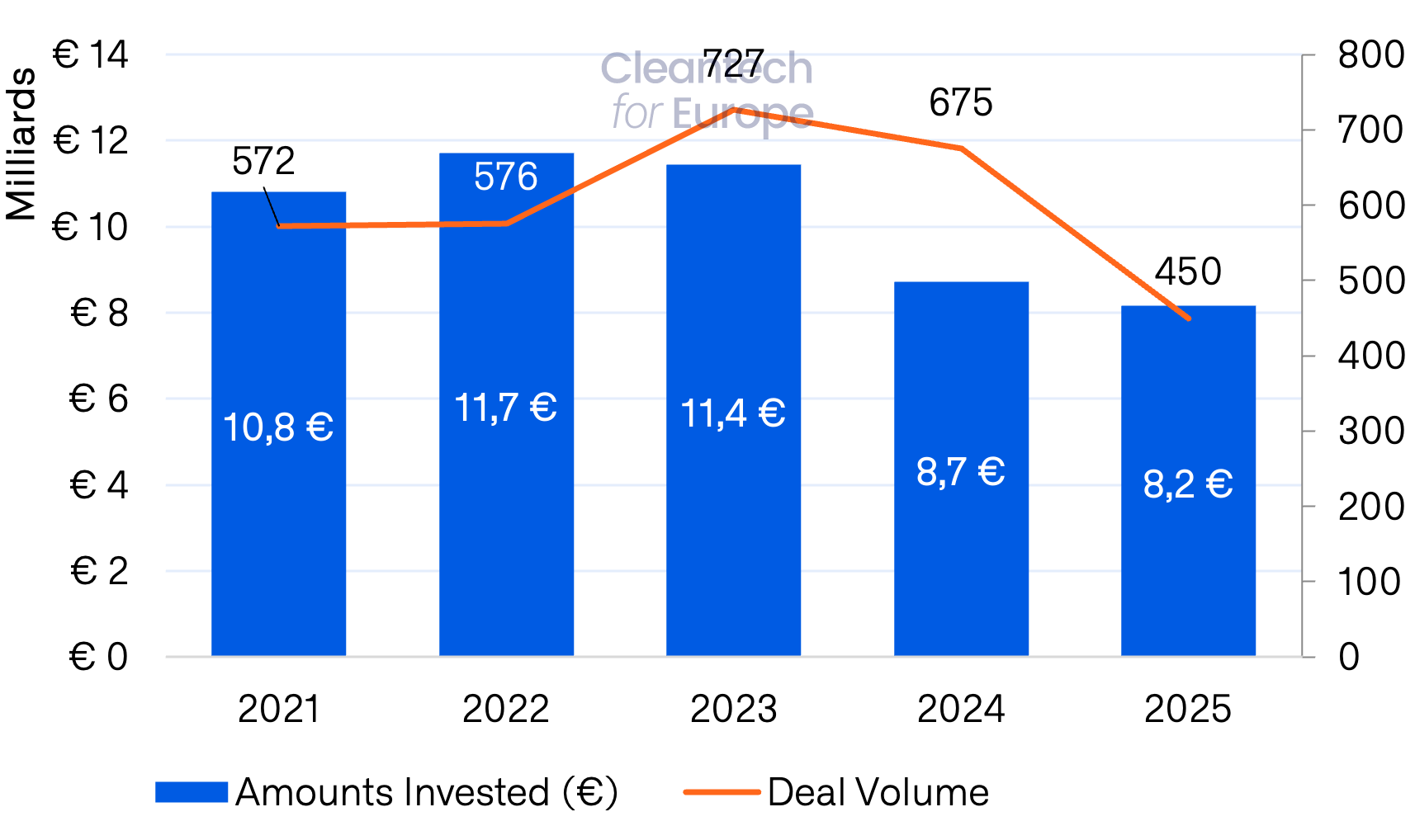

The data in this Annual Briefing confirms both Europe’s progress and its constraints. Europe continues to lead in clean technology innovation and early deployment, but 2025 marked a second consecutive year of declining venture and growth equity and persistent late-stage financing gaps, proving technologies is no longer the bottleneck. Scaling and manufacturing them in Europe is.

At the same time, the broader context has shifted decisively. Sovereignty has become a defining concern – economically, industrially, and geopolitically. Governments are reasserting control over energy systems, supply chains, and strategic industries; companies are seeking resilience against shocks; and trade is increasingly shaped by power rather than rules. China’s export-driven growth model, low domestic consumption, and dominance across key clean technology value chains continue to generate overcapacity and trade frictions, while both China and the United States openly pursue decoupling strategies.

Europe is only now fully internalising this reality. In 2025, that awakening became visible; in 2026, it must translate into action. Signals of a harder-edged approach are emerging – from the suspension of approval of the EU-US trade deal, to discussion of deploying the Anti-Coercion Instrument, to growing acceptance that reciprocity must matter in trade and industrial policy.

Europe remains open to the world, but it can no longer afford to be naïve. Many partners, including India, Brazil, and the United States, actively deploy industrial policy tools, including local content incentives, to build domestic clean industries. It is neither protectionist nor unreasonable for Europe to ensure that its public money supports strategic clean supply chains at home.

The stakes are rising. Energy-related supply chain security now extends beyond oil and gas to electricity systems, grids, critical raw materials, and cyber risks. The AI-driven data-centre boom is accelerating electricity demand and straining infrastructure, while creating strong demand pull for energy-efficient computing, liquid cooling, grid technologies, and clean baseload power. In parallel, investment momentum is building in critical raw materials, grids, geothermal, and technologies that de-risk supply chains and enable decentralised systems increasingly valued by industry and defence communities alike.

Policy developments in 2025 reflect this shift. The Clean Industrial Deal, the Industrial Accelerator Act, reforms to public procurement, the Electrification Action Plan, and debates on ETS, CBAM, and the Innovation Fund all point to growing recognition that decarbonisation, competitiveness, and resilience must be pursued together. Yet Europe still moves too slowly. Institutional fragmentation, procedural drag, and intra-EU competition continue to dilute impact and undermine strategic coherence.

Europe’s challenge is not a lack of power, capital, or innovation, it is the difficulty of organising them. Hesitation risks reinforcing a self-fulfilling cycle of fragmentation and perceived weakness. But recent experience also shows that firmness, unity, preparedness, and willingness to engage can shift outcomes when Europe acts together.

There is reason for cautious optimism. Clean technologies are increasingly outperforming fossil alternatives on cost and quality. In 2025, wind and solar generated more electricity than fossil fuels in Europe for the first time, and electric vehicles overtook internal combustion sales in December. These trends will continue. The question is whether Europe captures their industrial and economic value.

The choice ahead is clear. Europe must move beyond the fallacy that technological demonstration is the finish line. What matters is whether Europe can scale, manufacture, and deploy the clean technologies it invents and do so fast enough to compete in a harsher global order. Getting this right is not only about climate leadership; it is about industrial strength, economic security, and sustaining Europe’s social model.

Cleantech for Europe exists to support that effort by grounding policy in data and insights from the community of European cleantech companies and investors. The year ahead will test whether Europe can match its mindset shift with the speed and coordination the moment demands.

%20(1).jpg)

-min.png)

-min.jpeg)